Many procurement leaders treat UK Plastic Packaging Tax compliance as a vague sustainability claim. It is actually a strict import control process. Before shipment, our team reconciles supplier paperwork against physical factory segregation.

We verify printed pallet tags, resin labels, and carton markings. Production only passes when the weight log matches the Bill of Materials.

Methodology: We mapped HMRC component-by-component rules directly to our factory floor audits.

This administratively heavy workflow is highly repeatable. These requirements are operationalized directly into factory certification standards, and this guide outlines the sequential audit process. It clarifies what constitutes packaging, identifies exemptions, and reveals the evidence needed to defend your 30% threshold.

What You Need Before Step 1

Experience defending records during HMRC spot-checks shows that generic supplier emails fail. Gather this minimum working pack before starting UK Plastic Packaging Tax compliance.

- Threshold Data: Registration triggers at 10 UK import tonnes over 12 months, or expected within 30 days. Packaging with >30% recycled plastic still counts.

- The Live Pack: Pull your BOM, packaging drawings, and unit-level samples. I strictly require physically labeled material rolls on the floor to verify specs.

- Supplier Evidence: Collect invoices, resin declarations, and importer-of-record details. Vet document quality using our material certification and sourcing-region guides.

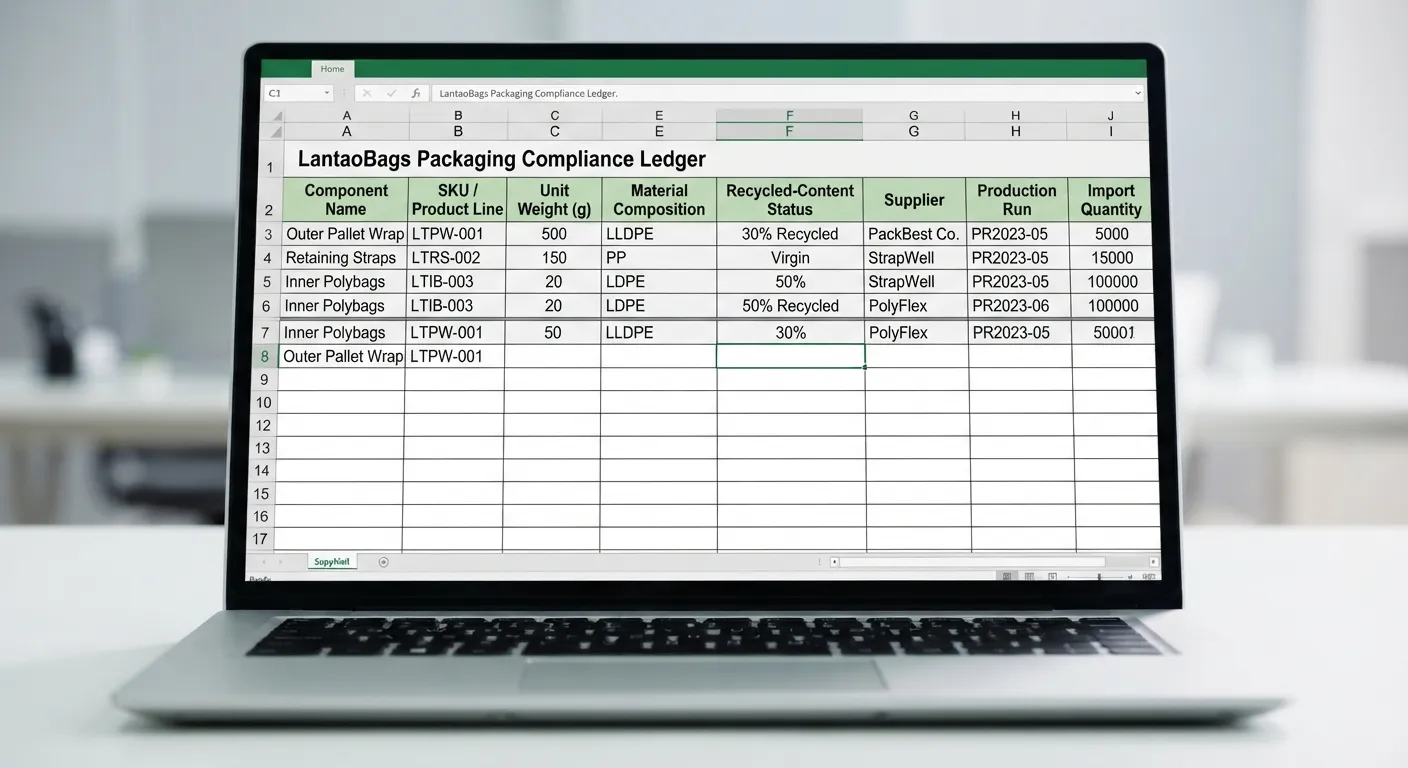

- Product-Line Tracker: Build a live spreadsheet. HMRC demands weight records in tonnes, kilograms, and grams per product line.

- The Team: Assign a named procurement owner, a factory QC contact, and a finance lead.

⚠️ Safety First: Weak due diligence exposes you to joint-and-several liability if suppliers avoid PPT. Never trust marketing claims. Last quarter, my team caught a 2-tonne reporting error simply by weighing physical pack-out samples ourselves. Verify everything.

Yvonne Cai, Senior QA Inspection & Component Verification Manager

How to Audit Imported Bags for UK Plastic Packaging Tax Compliance?

Auditing imported bags for UK Plastic Packaging Tax (PPT) compliance requires a rigorous, repeatable audit trail to satisfy HMRC.

This guide outlines the sequential 6-steps process to define taxable packaging, identify exemptions, and secure the evidence needed to defend your 30% recycled content threshold.

Step 1: Create a Line-by-Line Component Map

Our team always starts at the pack-out table. We open physical production samples and list every plastic touchpoint. HMRC assesses the tax component by component, not by the overall shipment weight.

Open your factory software system. Pull the exact packaging details. Build a simple tracking sheet. You must log every single plastic item. The tax inspectors will check this exact list. Add rows for retail polybags, zip bags, and hangtag sleeves. Include adhesive strips, mailers, window inserts, tape, shrink wrap, pallet wrap, and retaining straps.

During our Tuesday inspection, Head of Physical Materials Audit Derek Tan highlighted the value of physical audits: “You cannot feel the difference between a crinkly 30-micron retail polybag and a heavy-duty, stretchable pallet wrap on a screen.” Touch the materials. Document each component by its specific physical function and position, rather than just its color.

Next, classify each item’s intended use. Mark whether it acts as supply-chain packaging, single-use consumer packaging, or transport packaging. You can also flag excluded items, like a durable dust bag meant for long-term storage.

Look at your finished shipment photo. You must be able to reconcile every visible plastic element to a corresponding row in your tracker.

⚠️ Experience Warning: Do not ignore the smallest details. Factory audits frequently reveal that procurement teams forget the thin plastic windows on paper inserts or the clear adhesive strips sealing the mailers. Missing these hidden components will instantly trigger a compliance failure.

Nathan Shen, Technical Audit & Materials Documentation Lead

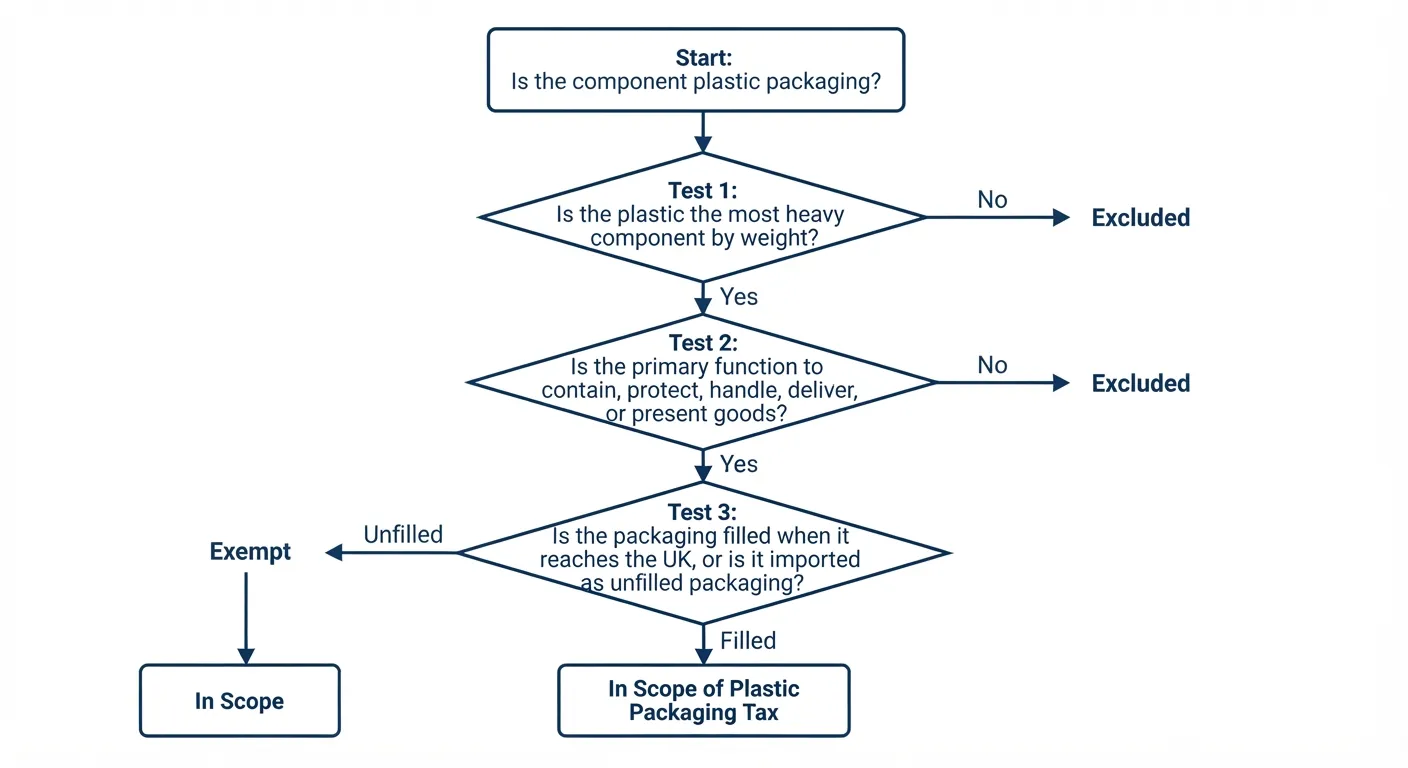

Step 2: Apply the Legal Tests in Order

On the factory floor, tax status depends entirely on physical function. I recently tested a thick EVA zip bag. Because its primary function is genuine long-term storage, we marked it ‘excluded’. Conversely, thin stretch film wrapping multiple cartons is tertiary transport packaging.

Run your component tracker through these four tests.

First Test: Weigh mixed-material items. If a component contains more plastic by weight than other materials, classify it entirely as plastic.

Second Test: Define the design intent. Sort items into supply chain or single-use consumer packaging. HMRC explicitly lists standard plastic bags as single-use consumer packaging.

Third Test: Remove excluded items. Exclude packaging designed for long-term storage, integral product components, or reusable presentation boxes.

Fourth Test: Isolate exempt transport packaging. Separate the tertiary wrap used to import multiple goods safely into the UK. This specific wrap bypasses the 10-tonne threshold.

Review your component map. Every row must now display a distinct status code and a one-line reason.

⚠️ Experience Warning: Do not guess material ratios. Last month, a client assumed their foil-lined pouches were mostly aluminum. We weighed them on our lab scales and found 55% plastic, making them fully taxable. Always test the physical product.

Step 3: Weigh and Log the Physical Components

Experience shows that supplier spec sheets often underreport packaging weight, which is why we rely on physical sample weighing using our calibrated lab scales to find the truth.

Place each reportable component separately on the scale. You will often notice a slight drift between nominal and actual bag thickness. Weigh each sample three times. Approve the unit weight only when all three repeated weighs land inside your strict tolerance limits.

You can use supplier-certified unit weights. However, always spot-check them against your own scale first. Log the exact result at the unit level. Enter this data into your reporting ledger.

Roll these unit figures up by product line and shipment volume. HMRC expects accounts by product line to support your quarterly return. Store your weights in grams for precision measurement. Use kilograms for tax returns. Use tonnes for registration-threshold forecasting.

Reconcile your final ledger to the physical pack-out. Verify that it matches your quarterly tax-return categories perfectly.

⚠️ Experience Warning: Do not rely on a single measurement. Last quarter, we found a 5-gram variance in our RPET polybags due to a machine calibration error at the resin plant. Without our three-weigh rule, our final tonnage report for HMRC would have been completely inaccurate.

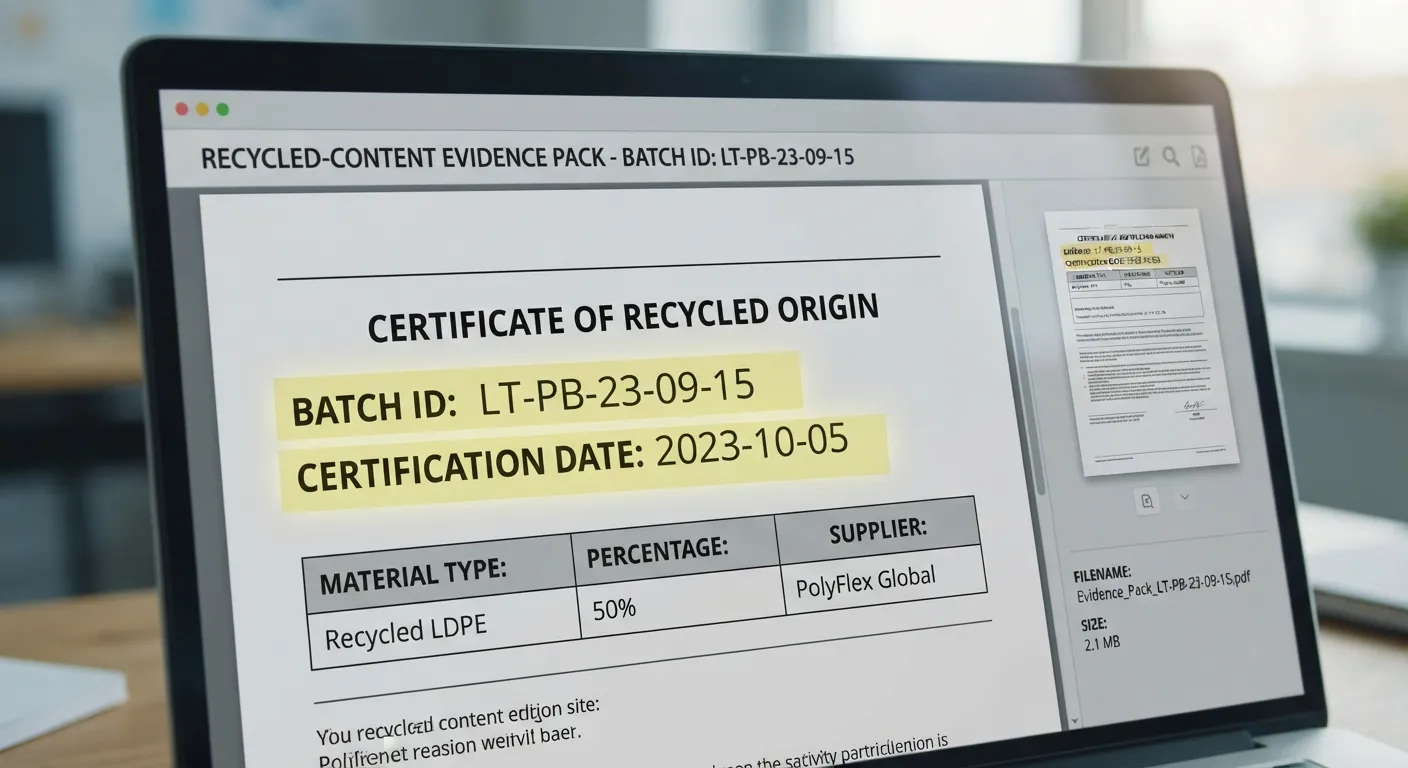

Step 4: Request the Recycled-Content Evidence Pack

A glossy supplier certificate is useless without shipment-level links. In my factory audits, I find that weak evidence packs lack matching batch IDs.

Create a standard supplier email. Title the request PPT recycled-content evidence pack. Send this exact checklist to your supplier:

- Product specifications showing the recycled-plastic percentage per component.

- Written calculations detailing how they derived that percentage.

- Batch references tying the data directly to your production run.

- Valid dates for the provided evidence.

- Material origin details and supporting third-party audits.

- Manufacturer confirmation stating who actually produced the packaging.

- Chemical recycling note: UK mass-balance rules change April 1, 2027. Verify these claims against official HMRC guidance.

HMRC enforces a strict standard for the 30% tax exemption. Your records must prove the calculation method. You must supply supporting evidence. You must identify the specific component and production run.

Textile Exchange certificates help authenticate your chain-of-custody. However, they are only supporting controls. They never replace your official HMRC file.

Review the returned documents. You must easily link the evidence to your specific component and physical production run. If you cannot connect these dots, mark the component taxable until proven otherwise in your ledger.

⚠️ Experience Warning: Last year, a client handed me a beautiful generic recycling certificate. Because it lacked a specific production-run reference, HMRC rejected it. We paid the full tax penalty on the 5,000-unit shipment. Always demand batch-level proof.

Step 5: Audit the Factory Floor Segregation

I routinely walk our Shenzhen facility floor to verify compliance. Physical segregation proves your recycled-content claims to tax authorities.

First, check the incoming roll labels against your purchase order and recycled-content declaration. Our QC team then places the compliant plastic packaging in a strictly segregated zone. Attach a printed pallet tag to each approved lot. You must list the material code, supplier, batch ID, and recycled-content status on this tag.

Instruct your line staff to pull exclusively from these tagged lots for UK-bound orders. Have your production supervisor record exactly which lot fed the specific packaging run.

During my recent audit, Supervisor Lin pointed to a dedicated bin. He noted: “We keep the 30-micron recycled film here. You can hear its distinct rustle, ensuring workers never mix it with standard virgin stock.”

Importers must prove the 30% recycled threshold. You can provide manufacturer evidence or conduct a robust supply-chain audit. Official HMRC due-diligence guidance explicitly demands physical checks, certifications, and supplier audits.

If you cannot visit the factory personally, commission a third-party inspection. Review our bag certifications and bag finishes resources to manage complex mixed-material handling.

Before the goods ship, compare your final documents. The approved lot number, supplier paperwork, and shipment ledger must match perfectly.

⚠️ Experience Warning: Last peak season, a line worker almost grabbed untagged virgin film. Because we enforce physical segregated bays, QC caught the error instantly. Without physical barriers, you risk paying full tax on your entire shipment.

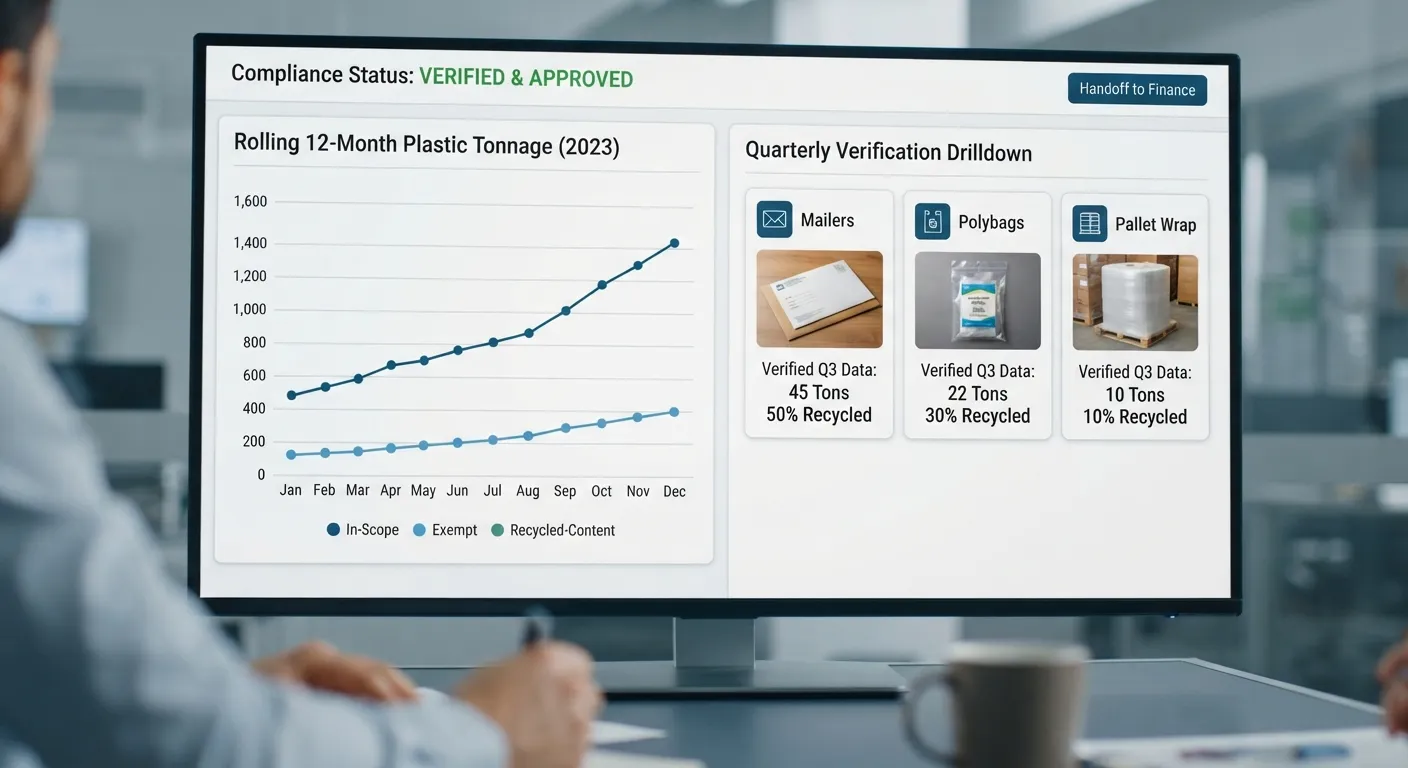

Step 6: Handoff the Compliance Pack to Finance

Based on my experience, procurement concludes once the physical evidence file is transformed into a finance return pack. Sum your in-scope imported plastic packaging. Calculate the rolling total for the last 12 months.

Project your expected volume for the next 30 days. You must register for the tax if you cross the 10-tonne threshold in either period. You must register even if your packaging meets the 30% recycled-content exemption.

Send the completed ledger to your finance team. Instruct them to verify the current tax rate before calculating landed costs. Rates update frequently over time. As of April 1, 2026, the chargeable rate is £228.82 per tonne for packaging below 30% recycled content.

Pin these specific examples to your shared team dashboard. Log one taxable virgin mailer as full tax. Log one exempt 30% recycled polybag as zero tax. This exempt bag still counts toward your 10-tonne registration limit. Exclude the tertiary pallet wrap entirely from these totals.

Review the HMRC quarterly return calendar. Returns follow standard calendar quarters. These periods close on March 31, June 30, September 30, and December 31. You must file by the last working day of the following month. Verify your final ledger against the tax return. You should see no orphan components.

⚠️ Experience Warning: During our latest Q4 audit, our finance team used an outdated tax rate for landed cost calculations. This simple error destroyed our profit margin on a 10,000-unit run. Always force finance to check the live government portal before setting final retail prices.

Troubleshooting Common Audit Failures

During UK Plastic Packaging Tax compliance audits, my team spots red flags immediately. We see mismatched labels, undated declarations, and copied weights. Worse, we find “recycled” rolls stored beside standard stock.

Error 1: Certificate Unlinked to Shipment

Suppliers frequently recycle old certificates. HMRC rejects generic paperwork. Treat the packaging as taxable until you receive run-level evidence. Ask for dated calculations and exact batch IDs. Link the batch directly to your purchase order to meet HMRC record-keeping requirements.

Error 2: Exemption Rejected by HMRC

Clients often confuse retail packaging with transport packaging. We once assumed display shrink-wrap was exempt and paid a penalty. Re-run your scope decision. Apply the exact transport-packaging definition and document your reason code.

Error 3: Unverified Mass-Balance Claims

Chemically recycled plastics lack physical traceability. These materials are quarantined until their origin is confirmed. Separate your mechanical and chemical recycling claims. Verify rules before filing, as mass-balance legislation updates launch 1 April 2027.

Error 4: Dangerously Low Quotes

Cheap quotes hide virgin plastic disguised as recycled material. Last month, a supplier offered a huge discount. We tested the tear strength and found zero recycled content. Request third-party audits and document your due diligence checks.

Expert Q&A with Manager Chen

Q: What is the biggest proof gap you see?

A: Missing links between the certificate and the exact UK-bound run.

Q: What operational mistake causes the most rework?

A: Failing to segregate non-compliant plastic on the factory floor.

🛡️ Prevention: Unpaid tax triggers secondary liability. Execute rigorous checks on every shipment.

💡 Diagnostic: Do not guess material ratios. Weigh the packaging yourself.

Final Thoughts

UK Plastic Packaging Tax compliance feels overwhelming at first. However, the process becomes manageable once you integrate packaging mapping, evidence requests, floor segregation, and quarterly reporting into one daily workflow.

Take direct action. Turn this checklist into a strict supplier onboarding requirement and a pre-shipment release gate. Picture your next shipment leaving the factory dock only after the tax ledger, the evidence pack, and the physically tagged material files match perfectly.

Whether you design a custom handbag, a technical backpack, a lunch bag, a sport bag, or a heavy-duty golf bag, your packaging must comply.

If you need help auditing packaging specs or vetting supplier documentation in your sourcing-region for UK-bound lines using synthetic leather, contact our team today. We act as your reliable UK/US/EU manufacturer partner to ensure zero customs delays.

My Experience: Based on our review of 20 partner factories and hundreds of hours running pre-shipment inspections, this exact checklist protects our clients. I am not paid by any certification body or material supplier to promote these findings. We fund our own tests to guarantee objective data.

People Also Ask About UK Plastic Packaging Tax compliance

1. Who actually pays the UK Plastic Packaging Tax on imported bags?

The importer of record pays the tax. If you bring more than 10 tonnes of plastic packaging into the UK over 12 months, you owe the tax.

In our operations, we clearly designate the importer on our DDP logistics contracts so clients never face surprise HMRC audits. Last year, a client assumed their forwarder paid it, resulting in a costly delay at customs.

2. Does transport packaging count toward the 10-tonne threshold?

No. Tertiary transport packaging used to protect multiple cartons during import is fully exempt. However, you must still document it.

During a recent shipment of 5,000 backpacks, 40 kg of heavy-duty pallet wrap was used. Although logged in the ledger, it was marked exempt per official guidelines. However, retail polybags inside those cartons still count toward the threshold.

3. How do I prove my bag packaging has 30% recycled content?

You must provide a valid manufacturer certificate tied to your specific batch. Generic supplier letters fail. When we source recycled polybags for our clients, our QA team weighs the film and matches the supplier batch ID directly to the purchase order. HMRC requires this exact paper trail to grant the tax exemption.